The HP Filter

Learning objectives¶

Understand trend–cycle decomposition

Interpret the smoothing parameter

Smoothing time series data is useful in many economic situations. The main idea is to try to separate a “trend” from a “cycle.” The smoothed series should not differ too much from the actual data. This is done through a choice of parameters in the filter.

Setup¶

Suppose we have observations on the log of some time series for , where consists of a trend term, , and a cyclical component, , so that .

The HP filter finds that solves

or, rewriting

¶

where is the ``smoothness penalty.‘’ Note that as , we just have the series, , itself and is just a regression on a linear trend (second difference is 0). Here is a Python implementation:

import numpy as np

import pandas as pd

import pandas_datareader as pdr

import datetime

from statsmodels.tsa.filters.hp_filter import hpfilter

import matplotlib.pyplot as plt

import matplotlib as mpl

from cycler import cycler

from tabulate import tabulate

from matplotlib.dates import DateFormatter

from pandas.plotting import register_matplotlib_converters

register_matplotlib_converters

import matplotlib.ticker as ticker

###from statsmodels.tsa.x13 import x13_arima_analysis

import sys

### Some libraries for web scraping (BLS revisions)

import requests

from bs4 import BeautifulSoup

import time

start_time = time.time()

pd.set_option('display.max_rows', None)

my_colors = ["#00688b",

"#cd3333",

"#6c8b3d",

"cornflowerblue",

"#cd6600",

"#8b2323",

"#5d478b",

"red"]

plt.rcParams['axes.prop_cycle'] = cycler(color = my_colors)

plt.rcParams['axes.spines.right'] = False

plt.rcParams['axes.spines.top'] = False

plt.rcParams['axes.xmargin'] = 0

#plt.rcParams['axes.ymargin'] = 0.0

plt.rcParams["figure.figsize"] = (10.5,6.5)

plt.rcParams['font.family'] = 'sans-serif'

plt.rcParams['font.size'] = 14

plt.rcParams['legend.fontsize'] = 'medium'

plt.rcParams['legend.frameon'] = False

plt.rcParams['legend.framealpha'] = None

plt.rcParams["legend.loc"] = 'best'

plt.rcParams['axes.titlesize'] = 'xx-large'

plt.rcParams['axes.titlecolor'] = '#3333B3FF'

plt.rcParams['lines.linewidth'] = 3

plt.rcParams['figure.subplot.left'] = 0

plt.rcParams['figure.subplot.bottom'] = 0

plt.rcParams['figure.subplot.right'] = 1

plt.rcParams['figure.subplot.top'] = 1

def crosscorr(datax, datay, lag=0):

return datax.corr(datay.shift(lag))

def NBER(start_date):

ax2 = ax.twinx()

Recessions = monthly['recessiondates'][monthly.index >= start_date]

ax2.fill_between(Recessions.index,

Recessions,

step="pre",

color="gray",

alpha=0.2)

ax2.get_yaxis().set_visible(False)

return ax2

def simpleaxis(ax):

ax.spines['top'].set_visible(False)

ax.spines['right'].set_visible(False)

ax.get_xaxis().tick_bottom()

ax.get_yaxis().tick_left()

def day_format(label):

"""

Convert time label to the format of pandas line plot

"""

return f'{label.month} {label.day}'

def month_format(label):

"""

Convert time label to the format of pandas line plot

"""

month = label.month_name()[:3]

if month == 'Jan':

month = month + '\n' + f'{label.year}'

#else:

# month = ""

return month

def quarter_format(label):

"""

Convert time label to the format of pandas line plot

"""

month = label.month_name()[:3]

if month == 'Jan':

month = f'Q1\n{label.year}'

if month == 'Apr':

month = 'Q2'

if month == 'Jul':

month = 'Q3'

if month == 'Oct':

month = 'Q4'

return month

Now we will read in some data.

### Quarterly

FREDmap = {

'GDPC1': 'real_gdp'

}

quarterly = pdr.DataReader(list(FREDmap.keys()), 'fred', datetime.datetime(1800,1,1))

quarterly.rename(columns = FREDmap, inplace = True)

quarterly.to_pickle('quarterly.pickle')

quarterly['real_gdp'].tail()DATE

2023-07-01 22780.933

2023-10-01 22960.600

2024-01-01 23053.545

2024-04-01 23223.906

2024-07-01 23386.733

Name: real_gdp, dtype: float64def EconLineGraph(dataframe = None,

series = None,

labels = None,

title = None,

subtitle = None,

source = None,

ylabel = None,

start_date = None,

end_date = None,

graph_name = None,

recessions = False,

logscale = False,

ylines = None,

yzero = False):

"""For creating line graphs from a data frame

Inputs:

-------

dataframe : dataframe

The dataframe containing the data to be plotted

series : vector of text

The "names" of the variables to be plotted

labels : vector of text

The labels (descriptions) of each variable

title : text string

Title for the figure

subtitle : text string

A "title" which appears at top left of the figure

source : text string

The source for the data; appears at bottom right of the figure

ylabel : text string

Text that appears beside the y axis

start_date : string

The first date to appear in the figure (end date is always the last available

observation). String as 'yyyy-mm-dd'.

graph_name : text string

The basename for the graph files. Both pdf and png files are produced

recessions : logical

If True, then include NBER business cycle recession shading from

the dataframe "monthly"

"""

if start_date == None:

df = dataframe[series].dropna(how = 'all')

start_date = df.first_valid_index()

else:

df = dataframe.loc[start_date:][series].dropna(how = 'all')

fig, ax = plt.subplots()

if logscale:

ax.set_yscale('log')

ax.yaxis.set_major_formatter(plt.FormatStrFormatter("%.0f"))

ax.yaxis.set_minor_formatter(plt.FormatStrFormatter("%.0f"))

if recessions:

ax.plot(df, clip_on = False)

else:

df.plot(ax = ax, clip_on = False)

if yzero is True:

plt.axhline(y = 0, color = '#a0a0a0', linewidth = 0.75, label = None)

else:

if ylines is not None:

if len(ylines) == 1:

df[str(ylines)] = ylines[0]

df[str(ylines)].loc[start_date:].plot(ax = ax, clip_on = False, color = '#a0a0a0', linewidth = 1.0)

else:

for i in ylines:

df[str(i)] = i

df[str(i)].loc[start_date:].plot(ax = ax, clip_on = False, color = '#a0a0a0', linewidth = 1.0)

if title is not None:

ax.set_title(title)

if subtitle is not None:

ax.set_title(subtitle,

loc = 'left',

color = 'black',

size = 'medium')

if ylabel is not None:

ax.set_ylabel(ylabel)

if labels is not None:

#if ax.get_legend() != None:

ax.legend(labels)

#ax.legend().set_zorder(2)

else:

if ax.get_legend() != None:

ax.legend().set_visible(False)

if source is not None:

ax.set_xlabel('Source: ' + source,

horizontalalignment='right',

x=1.0)

else:

ax.set_xlabel('')

if recessions:

ax2 = ax.twinx()

Recessions = monthly['recessiondates'][monthly.index >= start_date]

ax2.fill_between(Recessions.index,

Recessions,

step="pre",

color="gray",

alpha=.2)

ax2.get_yaxis().set_visible(False)

ax2.set_ymargin(0)

fig.savefig('pyfigs/pdf/' + graph_name + '.pdf', bbox_inches='tight', pad_inches=0.25)

fig.savefig('pyfigs/png/' + graph_name + '.png', bbox_inches='tight', pad_inches=0.25)

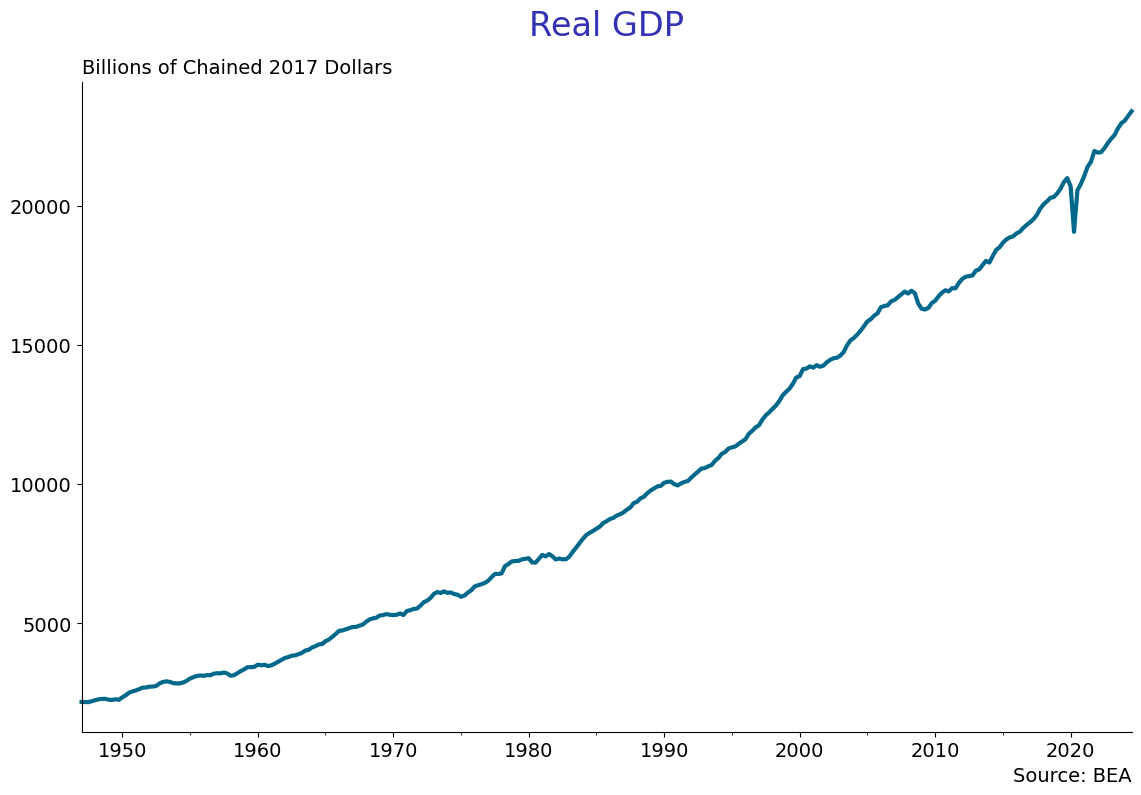

EconLineGraph(dataframe = quarterly,

series = ['real_gdp'],

title = 'Real GDP\n',

subtitle = 'Billions of Chained 2017 Dollars',

source = 'BEA',

start_date = '1947-01-01',

graph_name = 'log_real_gdp',

logscale= False)

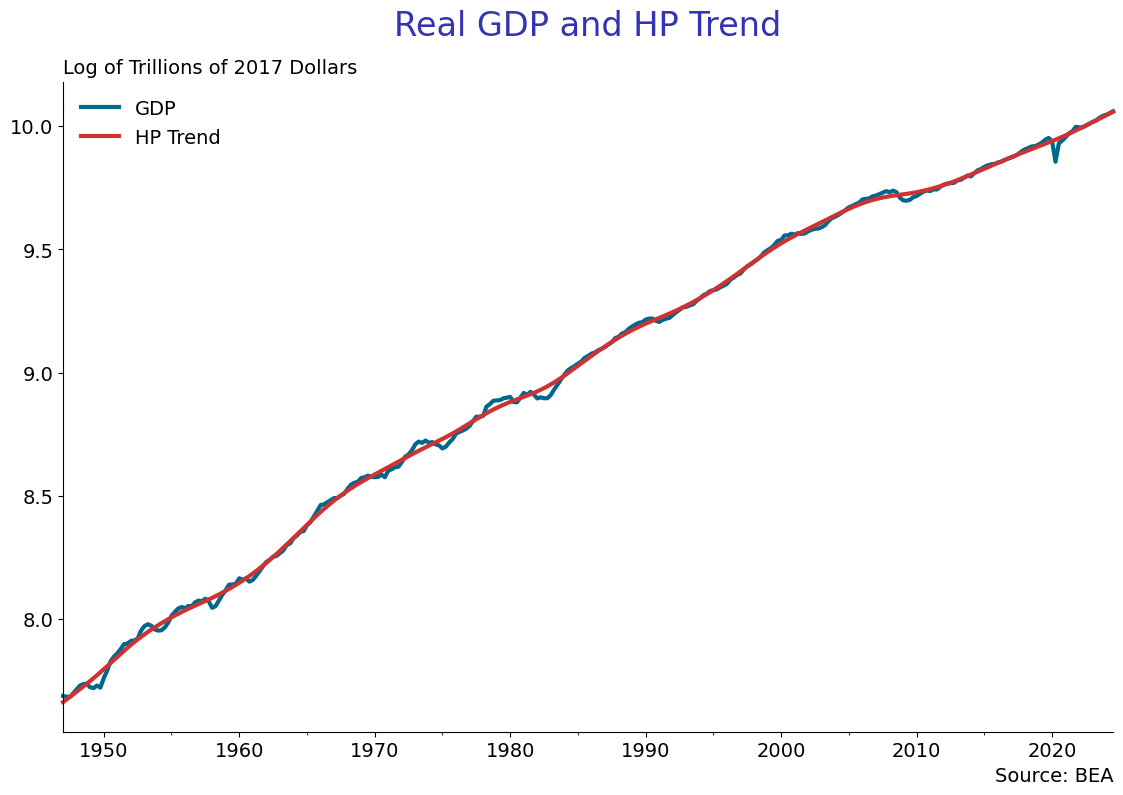

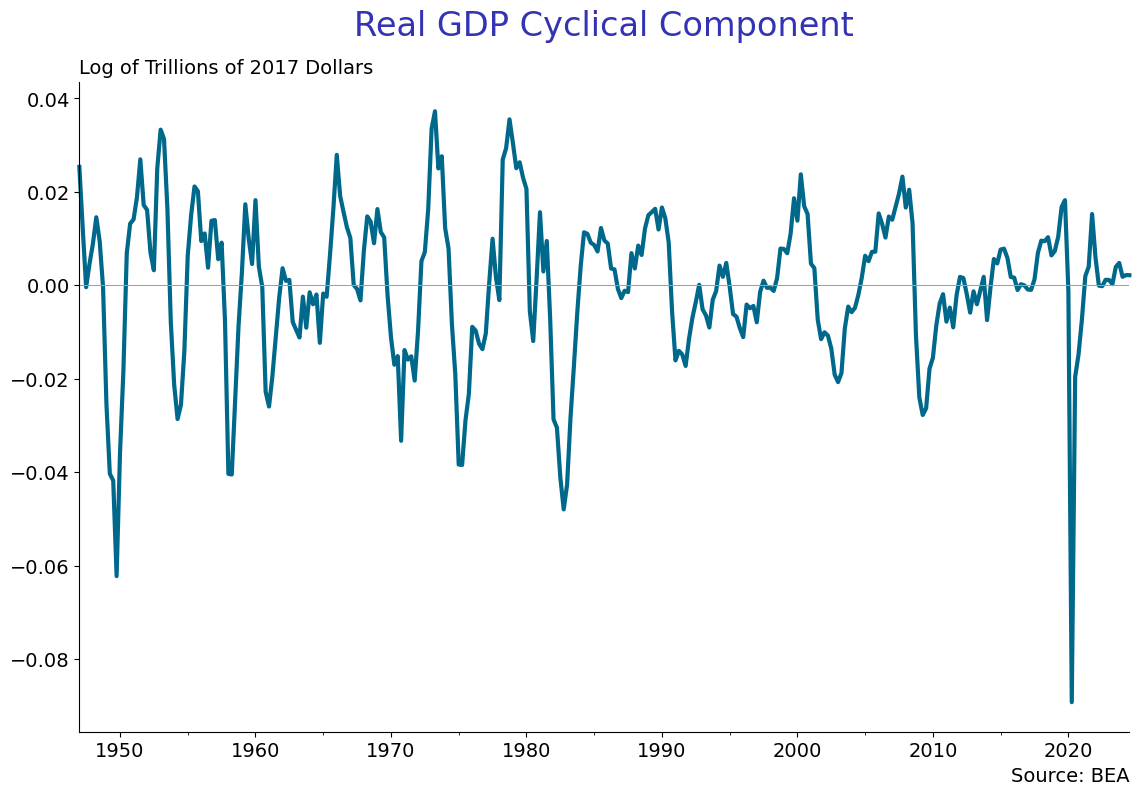

Take the log of real gdp and create the hpfilter, using 1600 for .

quarterly['lrgdp'] = np.log(quarterly['real_gdp'])

hpcycle_gdp, hptrend_gdp = hpfilter(quarterly['lrgdp'].dropna(), lamb=1600)

quarterly['hptrend_gdp'] = hptrend_gdp

quarterly['hpcycle_gdp'] = hpcycle_gdpNow graph the real gdp series and the hp trend.

EconLineGraph(dataframe = quarterly,

series = ['lrgdp', 'hptrend_gdp'],

labels = ['GDP', 'HP Trend'],

title = 'Real GDP and HP Trend\n',

subtitle = 'Log of Trillions of 2017 Dollars',

source = 'BEA',

start_date = '1947-01-01',

graph_name = 'hp_log_real_gdp',

logscale= False)

EconLineGraph(dataframe = quarterly,

series = ['hpcycle_gdp'],

title = 'Real GDP Cyclical Component\n',

subtitle = 'Log of Trillions of 2017 Dollars',

source = 'BEA',

start_date = '1947-01-01',

graph_name = 'hp_cycle_log_real_gdp',

yzero = True,

logscale= False)

Homework #1:

(A) Use a very large number for , like 16000000000 and see the trend and cycle. Explain what is going on. Next plot the cylical component for the two different ’s and comment on the difference.

(B) Download GDPCA from FRED. This is annual real GDP back to 1929. Should you use ? Why or why not? If not, what value should you use? Why?